PEARSON PLC ORD 25P PSON.L

PEARSON PLC ORD 25P PSON.L  DIAGEO PLC ORD 28 101/108P DGE.L

DIAGEO PLC ORD 28 101/108P DGE.L  RECKITT BENCKISER GROUP PLC ORD RKT.L

RECKITT BENCKISER GROUP PLC ORD RKT.L  LLOYDS BANKING GROUP PLC ORD 10 LLOY.L

LLOYDS BANKING GROUP PLC ORD 10 LLOY.L  MELROSE INDUSTRIES PLC ORD GBP0 MRO.L

MELROSE INDUSTRIES PLC ORD GBP0 MRO.L  FRESNILLO PLC ORD USD0.50 FRES.L

FRESNILLO PLC ORD USD0.50 FRES.L  NATWEST GROUP PLC ORD 107.69P NWG.L

NATWEST GROUP PLC ORD 107.69P NWG.L  WEIR GROUP PLC ORD 12.5P WEIR.L

WEIR GROUP PLC ORD 12.5P WEIR.L  STANDARD CHARTERED PLC ORD USD0 STAN.L

STANDARD CHARTERED PLC ORD USD0 STAN.L  ENDEAVOUR MINING PLC ORD USD0.0 EDV.L

ENDEAVOUR MINING PLC ORD USD0.0 EDV.L  OCADO GROUP PLC ORD 2P OCDO.L

OCADO GROUP PLC ORD 2P OCDO.L  ANGLO AMERICAN PLC ORD USD0.549 AAL.L

ANGLO AMERICAN PLC ORD USD0.549 AAL.L  BAE SYSTEMS PLC ORD 2.5P BA.L

BAE SYSTEMS PLC ORD 2.5P BA.L  VODAFONE GROUP PLC ORD USD0.20 VOD.L

VODAFONE GROUP PLC ORD USD0.20 VOD.L  HSBC HOLDINGS PLC ORD $0.50 (UK HSBA.L

HSBC HOLDINGS PLC ORD $0.50 (UK HSBA.L  GLENCORE PLC ORD USD0.01 GLEN.L

GLENCORE PLC ORD USD0.01 GLEN.L  UNITE GROUP PLC ORD 25P UTG.L

UNITE GROUP PLC ORD 25P UTG.L  CRODA INTERNATIONAL PLC ORD 10. CRDA.L

CRODA INTERNATIONAL PLC ORD 10. CRDA.L  KINGFISHER PLC ORD 15 5/7P KGF.L

KINGFISHER PLC ORD 15 5/7P KGF.L  TAYLOR WIMPEY PLC ORD 1P TW.L

TAYLOR WIMPEY PLC ORD 1P TW.L Since the beginning of the war in Ukraine, gas imports into the EU have significantly decreased. Azerbaijan’s significance has increased accordingly.

One of the oldest oil booms in the world is located on the Absheron Peninsula of Azerbaijan, which juts out into the Caspian Sea. Before drilling ever started, petroleum was manually extracted from the ground. With the Cop29 climate summit coming up in November, Baku is getting ready for a new era in energy. However, at the moment, Azerbaijan’s gas is more important than either oil or renewable energy, with Adnoc and Masdar emerging as significant allies.

Gas is exported by pipeline to Europe from four major countries: Iran, Algeria, Azerbaijan, and Russia. Since late 2021, Russia has essentially written itself out of the market, but some gas still passes through Ukraine. It is improbable that the contract will be extended when it ends at the end of this year.

Since Tuesday, Ukrainian forces have advanced into Russia and taken control of the Sudzha gas transit site, surprising Moscow. Even if Ukraine had the option to stop the gas supplies, doing so runs the danger of infrastructural damage or reprisal from Russia.

Through underwater pipelines, Russia continues to be a significant supplier to Turkey. Additionally, Russian gas reaches the European continent from Turkey.

Algeria and Iran, whose exports are hindered by a combination of political unrest, growing domestic consumption, and underinvestment in new manufacturing.

Pipelines connect Azerbaijan’s offshore fields to Erzurum, in eastern Turkey, via Georgia.

From there, part of the gas is sold into the Turkish market, and some is sent to western Turkey via the Trans-Anatolian Pipeline (Tanap), which opened in 2018 and connects to the Trans-Adriatic Pipeline (Tap), which stretches from Greece through Albania and Italy.

Since Azerbaijan contributes roughly 1 billion cubic meters per month to Turkey’s total monthly imports, which vary from 3 billion cubic meters in the summer to 6 billion cubic meters in the winter, Turkey has come to rely more and more on Azerbaijan.

Since the beginning of the war in Ukraine, gas imports into the EU have significantly decreased. Azerbaijan’s significance has increased accordingly; now, it supplies roughly 4% of the bloc’s imports, which is marginally less than the remaining Russian gas via Ukraine.

Gas prices in Europe have been declining since 2022 and have been mostly constant since the middle of 2023. Even yet, they are still significantly higher than they were before the crisis, averaging over $11 per million British thermal units, compared to an average of roughly $7 in 2018-19.

Unusually for the summer, they have recently hit their highest level since December 1. This is a result of security concerns, maintenance on some systems in Norway, competition with Asia for LNG supply, and increased air conditioning in response to heat waves. Further hurricanes that hit the US Gulf of Mexico could cut off LNG supplies, and the Houthi attacks have essentially closed the Red Sea, making it more difficult to get LNG from the Middle East to Europe.

As a courtesy to Hungary and Slovakia, who continue to depend on that route and are interested in the Kremlin, the EU intends to continue using the transit through Ukraine. Making an agreement with Azerbaijan to send its gas through Russia, or at the very least to exchange some Azeri gas for Russian, is one idea. While there would still be transit costs, there is an appeal for the EU and Ukraine to stop paying Moscow.

This agreement may be jeopardized by the violence in the Sudzha area. As opposed to the 12 billion cubic meters of Russian gas that passed through Ukraine last year, Azerbaijan can only supply an additional 2 billion cubic meters, according to the official gas company of Ukraine.

This emphasizes how difficult it will be for the EU to depend more on Baku. Since the last ten years, Azerbaijan’s domestic gas consumption has increased at a rate of roughly 5% yearly due to the country’s restricted gas production.

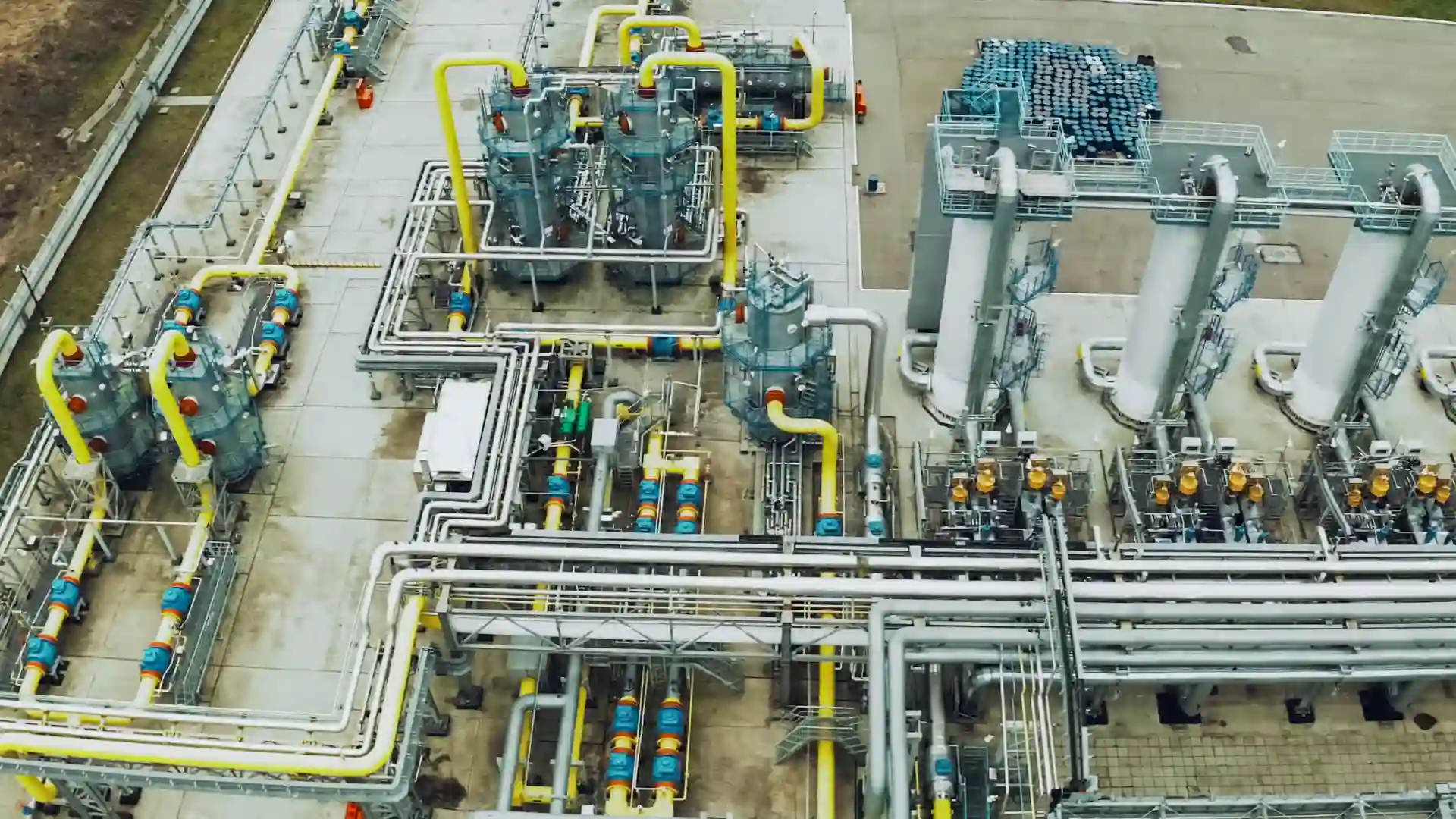

The corporations based in Abu Dhabi step in at this point. About 100 kilometres southeast of the peninsula bearing the same name, the vast offshore gas accumulation known as the Absheron field started production in July of last year. For the domestic market, the first phase produces 1.5 billion cubic meters annually; the second phase is expected to increase output to 5.5 billion cubic meters. The current partners, the French corporation TotalEnergies and the Azeri state company Socar, sold Adnoc a thirty per cent stake last August.

Along with an agreement with BP in Egypt, this was one of the Abu Dhabi corporation’s first international gas deals and provided them with a position in the gas supply to Europe. There may be room for cooperation on other possible gas projects that BP and Socar have.

The largest gas field in Azerbaijan and the primary source of its current exports, Shah Deniz, is managed by BP and is located immediately to the east of Absheron. In an effort to safeguard its gas supply, the Hungarian state electrical utility MVM purchased 5% of Shah Deniz from a joint venture between the Azeri government and Socar in June.

Another option to increase Azerbaijan’s supply is to transport gas from Turkmenistan, its neighbour to the east across the Caspian Sea. Turkmenistan has the fourth-largest reserves in the world, but there aren’t many export markets. The inaugural meeting of Central Asian energy ministers took place in Kazakhstan on Tuesday; however, only the ambassador of Turkmenistan and the deputy minister from Azerbaijan were present to represent their respective nations.

The two countries decided to work together to develop the Dostluk field in the Caspian in 2021, which might open the door for a cross-border gas pipeline. Turkey and Azerbaijan decided to cooperate to permit gas imports from Turkmenistan in June.

Additionally, Masdar and Azerbaijan have been collaborating on wind, solar and hydrogen project development. It completed a 230 megawatt solar farm in October, and in June it began construction on a 1 gigawatt solar and wind farm. These ought to partially offset household gas usage.

Azerbaijan also requires additional export capacity because Tanap and Tap are almost full. Because of its net-zero carbon targets, Europe has been hesitant to expand them, but it will need to make long-term commitments to purchase gas. Future hydrogen supply promises could ease Brussels’ consciences.

{kind=link}